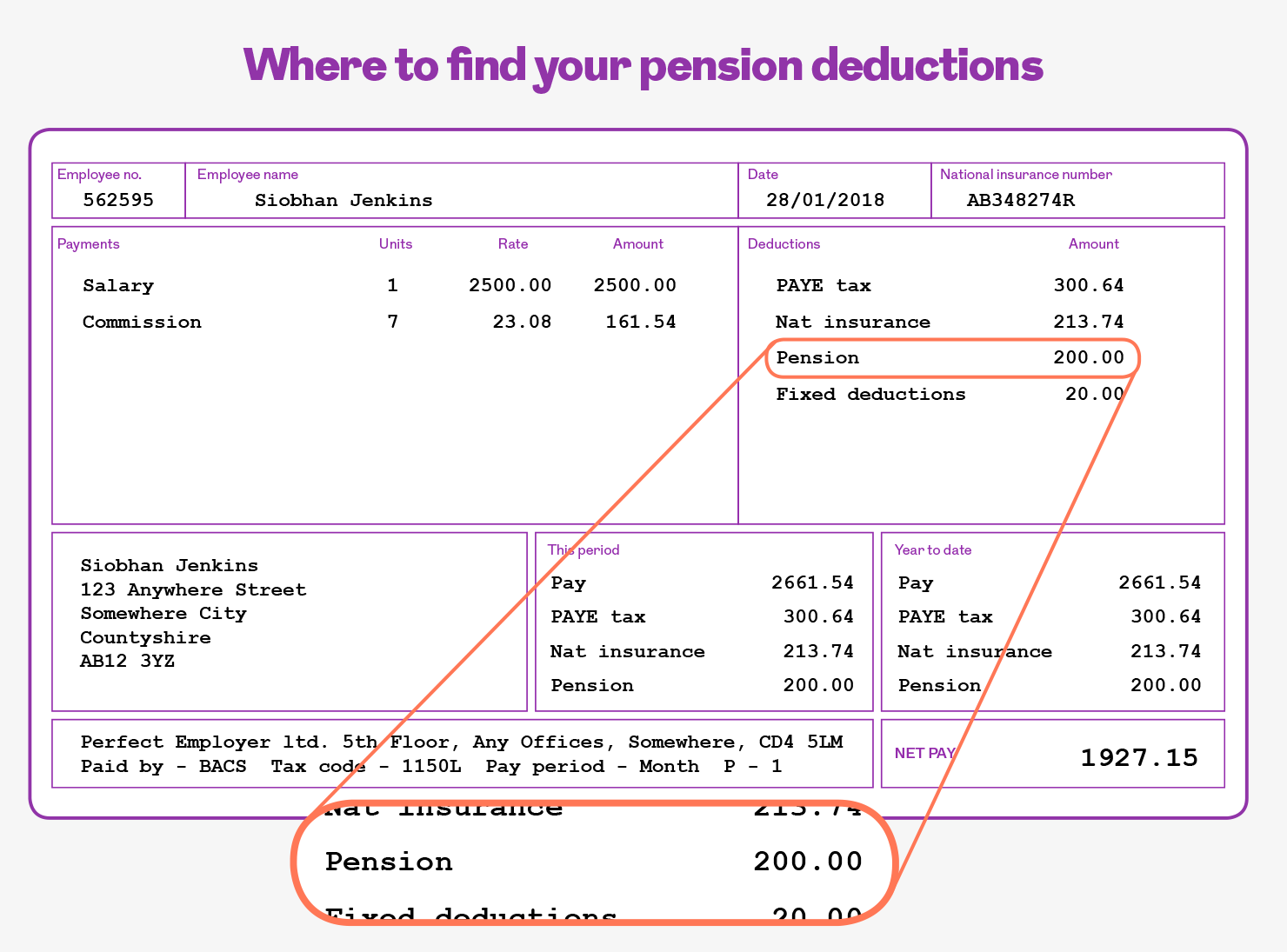

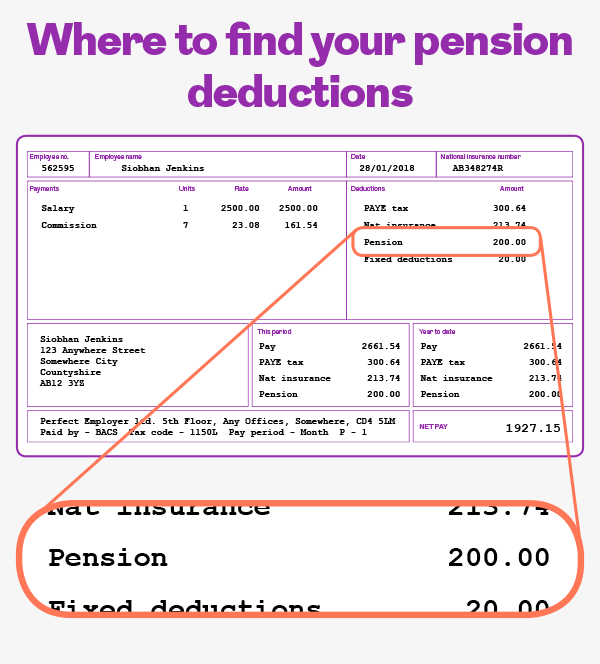

How to read your payslip: pension deductions

Your payslip often shows a deduction for a contribution into a pension scheme. But how is it worked out and what effect does it have on your tax bill?

Sometimes the information in your payslip can be difficult to get your head around. We’ve already explained how to understand the information when it comes to income tax and your tax code, and National Insurance Contributions (NICs), and this time we’re looking at pension deductions.

Firstly, it’s worth remembering that there are two main types of pension:

- Defined Benefit (DB) or ‘salary-related’ pensions, where the amount you get at retirement depends on how much you earned and how long you were a member of the scheme; and

- Defined Contribution (DC) pensions, where your contributions are invested until you start accessing your retirement savings.

In both cases, it’s quite normal for an employer to make a contribution into your pension in addition to your contribution. Although the contribution your employer makes may not be shown on your payslip, it’s a great way to help boost your retirement savings.

How do DB pension deductions work?

When it comes to the employee contribution, if you’re a member of a DB pension scheme, your payslip will show a deduction. This is simply the amount the scheme requires you to contribute to be a member of the scheme. In many schemes, this is a simple percentage of your salary. In the public sector, this percentage is generally higher for higher earners.

When you save into a pension, you usually benefit from a tax break. If you’re a member of a DB scheme, your pension contribution is taken from your gross wage, i.e. before you pay any tax. This reduces your taxable income, and therefore the amount of tax you pay.

For example, if you’re expected to contribute £100 per month into your DB pension scheme, your payslip will show that £100 figure. But when your tax bill is worked out, your income for tax purposes will be £100 lower than for someone who isn’t in the pension scheme. If you’re a standard rate (20%) taxpayer, this means that you will pay £20 less tax. If you pay tax at the higher (40%) rate, then your tax bill will be £40 less.

How about DC pension deductions?

If you’re a member of a DC pension scheme, there are two ways in which your contribution could be going out of your pay packet and into your pension scheme.

If you’re a member of a group personal pension, your pension contribution will come out of your take-home pay. Pensions benefit from tax relief, so if you want to contribute £100 to your pension every month, you only need to contribute £80, as the taxman will contribute the other £20. This is called tax relief. If you’re an intermediate rate (Scottish taxpayers only), higher rate or additional rate taxpayer, you could be entitled to claim more tax relief through a self-assessment tax return, or by contacting your local tax office.

Alternatively, if you’re a member of a DC occupational pension scheme, the pension contribution on your payslip is usually deducted before you pay any tax, as with a DB scheme. In this case, you get all the tax relief straight away – so there’s no need to make any further claim. If you’re a lower paid worker (e.g., under the tax threshold) you won’t receive tax relief.

What about salary sacrifice?

Many employers also offer something called ‘salary sacrifice’ or ‘salary exchange’. This is when you agree to take a slightly lower level of pay and, in return, your employer pays all of the pension contribution. The advantage of this arrangement is that no NICs are payable by you or your employer.

In such an arrangement, it’s possible that even though no deduction for pension is shown on your payslip, you’re still a member of the pension scheme. But normally there would be some indication on your payslip that a reduction in gross pay has taken place as part of a ‘salary exchange’ arrangement.

If you don’t understand the pension figure on your payslip, it’s worth asking your Human Resources department, payroll department or pension provider so you can make sure everything’s in order.

Related content

How to read your payslip: National Insurance

When it comes to your payslip, it’s useful to understand the different deductions from your salary, such as National Insurance

MORE

How much do you know about your credit score?

If you want to be accepted for credit, whether it’s a credit card or a loan, your credit score really matters. Take our quiz to find out how much you know about yours

MORE

How to read your payslip: tax codes

Your payslip can be difficult to get your head around, especially when it comes to understanding your tax code

MOREMore for you

Where does your tax go?

We all know we have to pay taxes, but do you know how they’re spent? Test your knowledge with our tax challenge

MORE

Five reasons to stay in your workplace pension

There are a number of important benefits you could lose if you choose to opt out of your workplace pension scheme

MORE

Your Q3 2018 outlook

Trevor Greetham, Head of Multi Asset Investments at Royal London, explains how the slowing global economy, alongside rising inflation and interest rates, could impact your money in Q3 2018

MORE