Why is making a will important?

If you don’t make plans on how you want to distribute your wealth once you’re gone, you may leave a host of problems behind

A well written will can give you the peace of mind that your loved ones will be looked after financially when you die.

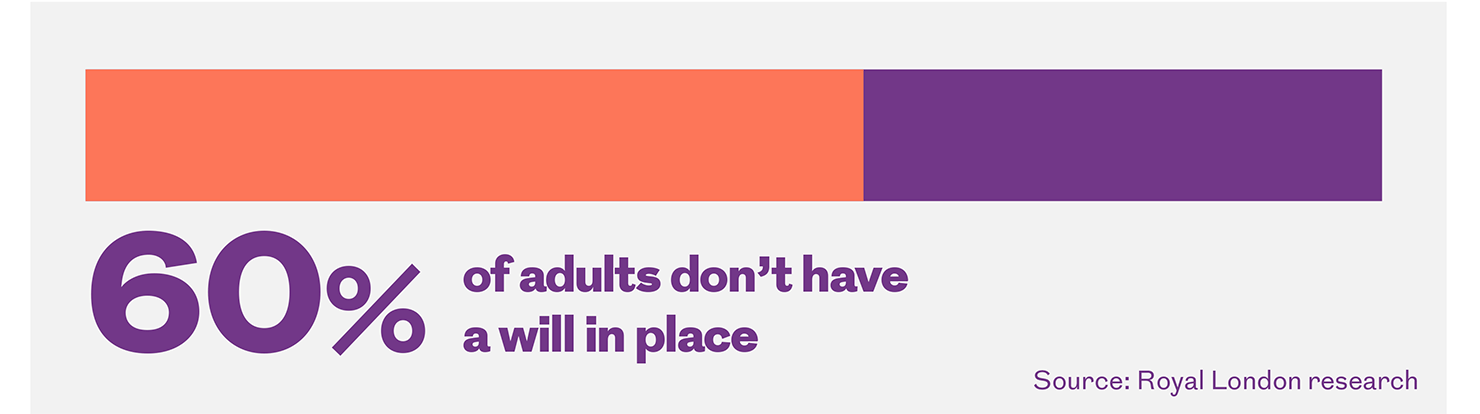

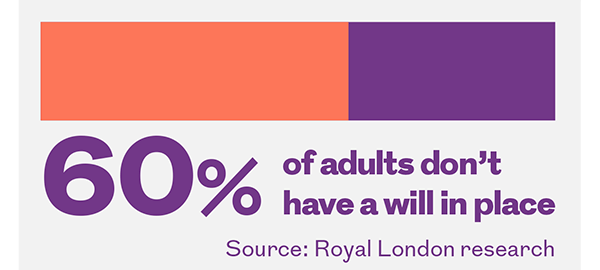

However, while this is one of the most important financial decisions anyone can make, research from Royal London shows 60% of adults haven’t made a will.

If there’s no will in place, your assets will be allocated according to UK law rather than your wishes – so setting them down in a legal format is very important. This is particularly the case for cohabiting couples, or people who’ve been separated or divorced. If you’re in a new relationship but haven’t updated your will, your current partner and children could end up with nothing.

How to make your will

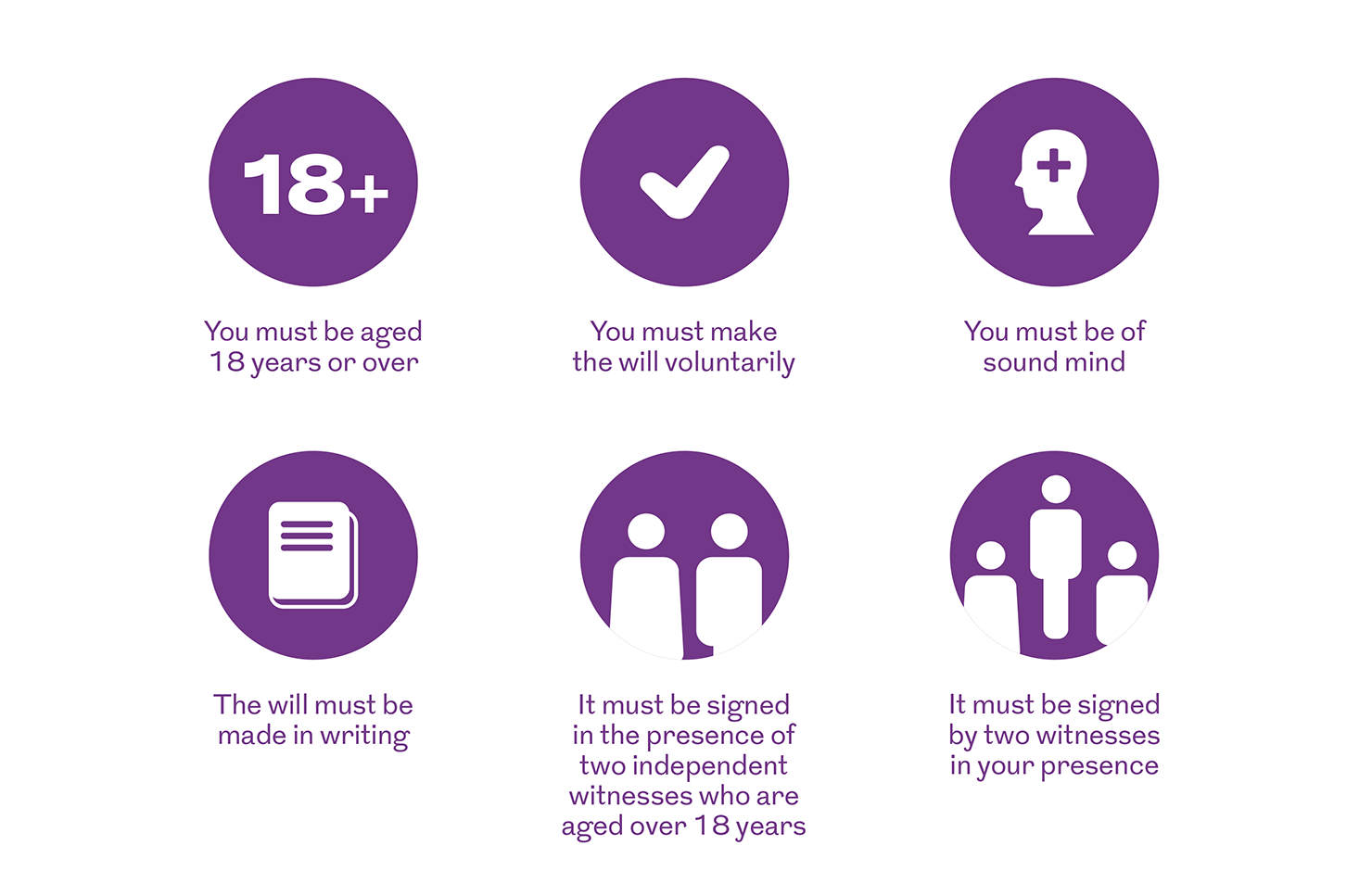

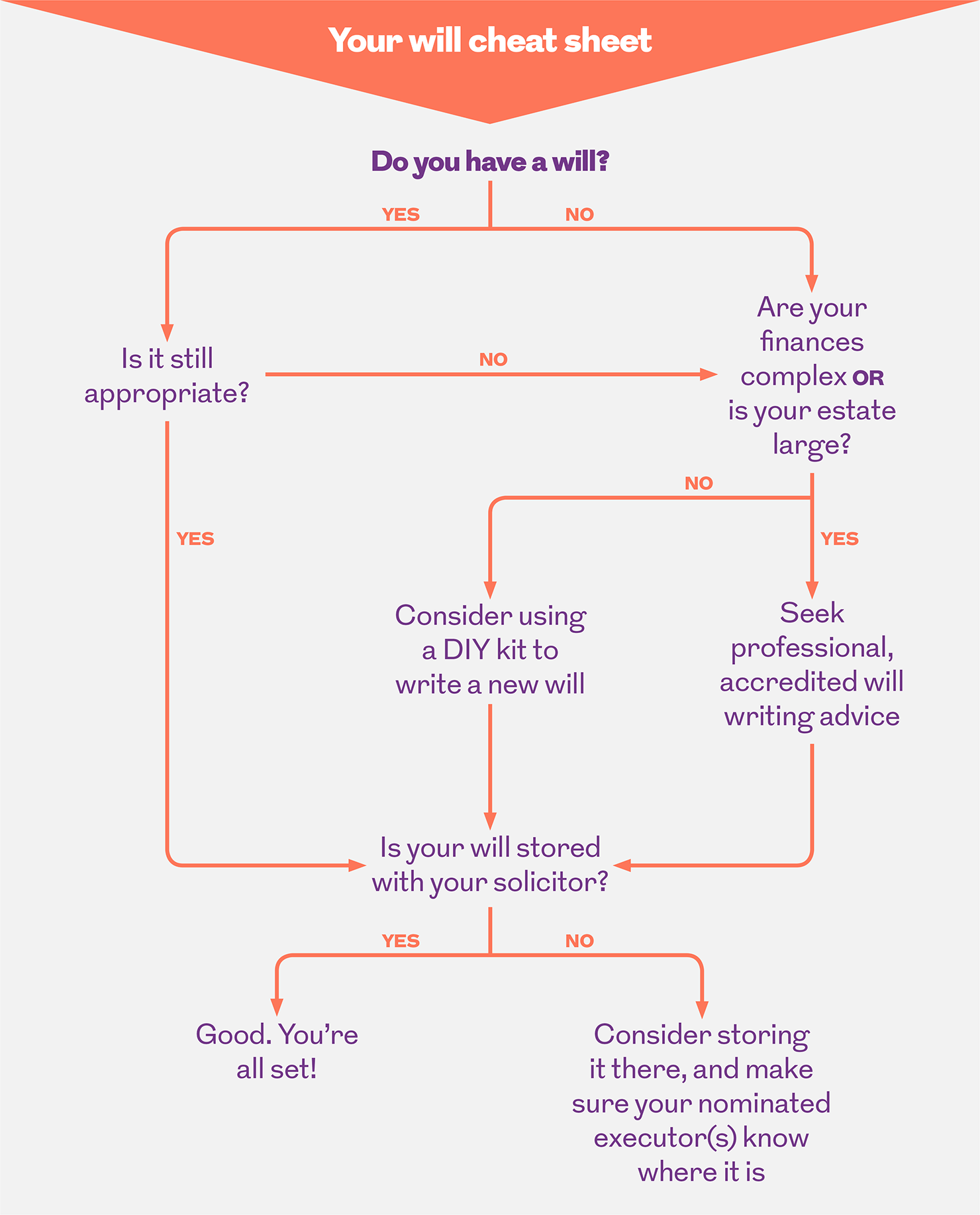

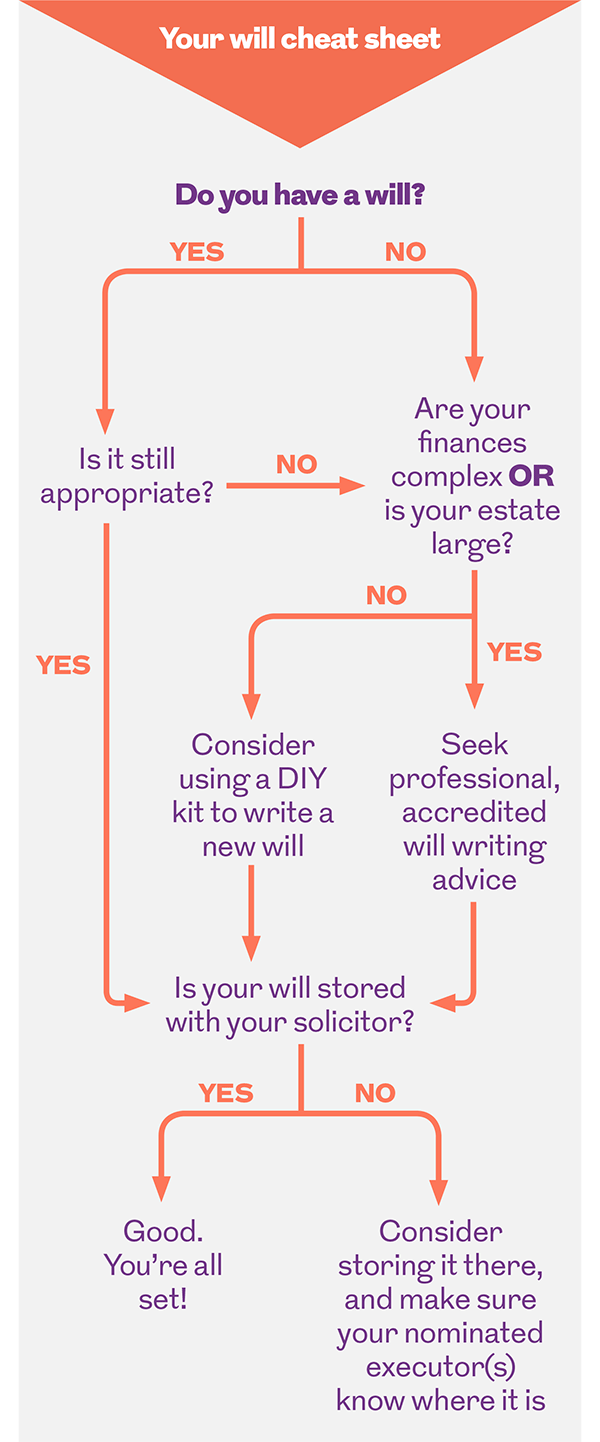

There are several options for making a will. The cheapest option is the do-it-yourself will, which can be bought online or at a stationer. While this might work if you have very simple financial affairs, there are important rules that must be followed for a will to be valid.

If you have more complicated financial affairs, it might be worth either visiting a will writing service, or having your will written for you by a solicitor. However, unlike solicitors, will writers may not be legally qualified, so it’s worth finding a will writer accredited by a body such as the Society of Will Writers.

Visiting a solicitor is the more expensive option, but if your affairs are complex, such as needing to do inheritance tax (IHT) planning or dealing with property overseas, then it’s worth paying the extra money.

Before you start

Before you write your will it’s worth taking some time to think about what you really want. Who do you want to leave your assets to and how? While some family members may be responsible with money, others may not, or you may want to leave something to children. In these cases, you might want to set up a trust arrangement for some beneficiaries, while others will receive gifts of money or possessions.

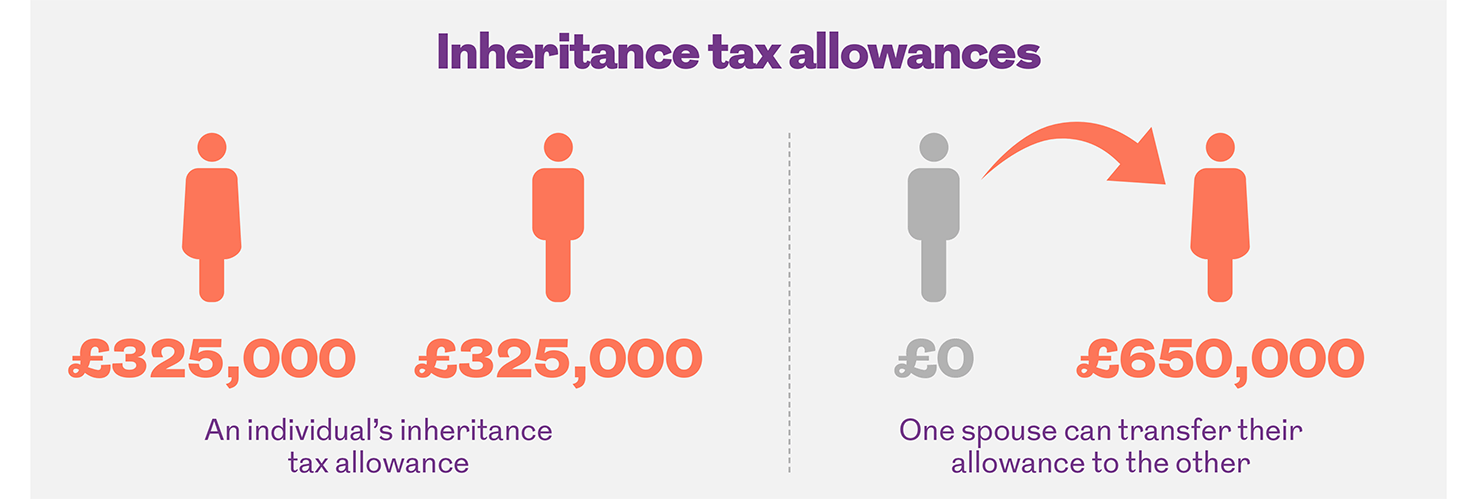

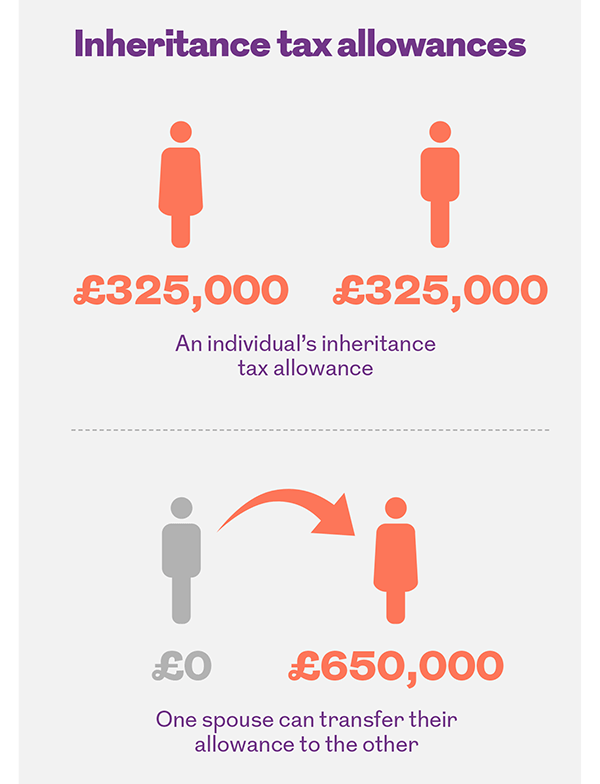

You should start by making a list of your assets and how much you think they’re worth. This should alert you to any potential IHT issues. When anyone dies, the first £325,000 of their estate is free from IHT – this is what’s known as your nil rate band. In most circumstances, you’ll have to pay IHT on anything over this amount.

However, if you’re leaving all your assets to your spouse or civil partner, there’s no IHT to pay. Your spouse or civil partner can also inherit your nil rate band if you die before them, giving them a nil rate band of up to £650,000.

People can also benefit from the use of a residential nil rate band (RNRB), which was introduced in April 2017. This means the first £100,000 of your home’s value is also free from IHT. However, this is dependent on you passing your home to a “direct descendant” such as your child or grandchild.

Like the IHT nil rate band, the RNRB can be transferred between spouses and civil partners. It’s currently £100,000, but will rise by £25,000 every year until it hits £175,000 in 2020/21. This means that by 2020/21 married couples and civil partners can get an IHT allowance of up to £1 million.

However, it’s worth remembering that wealthier people may not see any benefit from the RNRB because, for every £2 that the deceased’s net estate exceeds £2 million, it’s reduced by £1.

You also need to think about who you want to act as your executors – the people who take charge of dealing with your estate and distributing your assets. This is a hugely responsible position, which involves gathering your assets, paying any debts and making sure your assets are given to the people you mention in your will. You must trust the people you choose as your executors and make sure they’re comfortable in carrying out these duties.

Writing and updating wills

Wills must be written and witnessed as outlined above. If not, the will could be invalid and the assets may not be given to the people you wanted.

As personal circumstances can change quickly, it’s important to review and update your will regularly. For example, wills must be updated if you get separated, divorced or re-married. If you have children, the will should also be looked at. To avoid confusion, any old wills must be destroyed. It’s a good idea to store your will with your solicitor and let your executors know where they can find it if needed.

Related content

Why is life cover a good option further down the line?

If you have loved ones that depend on you, taking out life insurance can help to protect them in a number of different ways

MORE

Five ways to take your pension pot

The options for using your pension pot are more flexible than ever. But it’s important to understand how your decisions will affect your retirement income in the future

MOREMore for you

Getting the right mix for your pension

Lorna Blyth, Investment Strategy Manager at Royal London, and Trevor Greetham, Head of Multi Asset Investments at Royal London, tell you why a mix of investments is important to help grow your pot and reduce risk

MORE

Get more involved in your local community

There are lots of easy ways to support your community, from volunteering with a charity to helping out in a local school, or visiting an elderly neighbour

MORE

Your Q3 2018 outlook

Trevor Greetham, Head of Multi Asset Investments at Royal London, explains how the slowing global economy, alongside rising inflation and interest rates, could impact your money in Q3 2018

MORE